Unlock Financial Peace With Balance Confirmation In Finance

It is an irrefutable fact that accuracy and reliability are paramount in the finance and accounting domain. Businesses employ various auditing procedures to ensure the veracity of financial statements and strengthen the trust of stakeholders. One such crucial process is balance confirmation, which plays a vital role in validating the accuracy and completeness of recorded balances. Companies can obtain essential feedback on their financial transactions by exchanging information with external parties, such as customers, suppliers, or financial institutions.

This article shall act as a comprehensive guide that sheds light on the benefits and importance of balance confirmation in financial transactions. We will explore how this process enhances the integrity of financial statements, helps detect errors or discrepancies, and promotes transparency and accountability. Furthermore, we will understand the role of automating the balance confirmation process of your company to improve your overall accounting efficiency.

What do you mean by balance confirmation?

Balance confirmation denotes a process used in accounting to check the precision and completeness of the balances recorded in a company’s financial statements. It typically involves exchanging information between a company and its external stakeholders, such as customers, suppliers, or financial institutions.

During the balance confirmation process, a company will send out balance confirmation requests to its stakeholders, requesting them to confirm the balances they hold or owe to the company. These requests are typically sent in writing through a balance confirmation letter, email, or online platform. The balance confirmation process is commonly used across various industries, including manufacturing, retail, banking, and services. It is particularly essential in industries with significant accounts receivable or accounts payable balances, where confirmation helps validate the accuracy of these balances.

Benefits & Importance

Balance confirmation holds significant importance in finance for several reasons:

- Upholding Accuracy: Account Confirmation helps verify the accuracy of financial records by reconciling them with the records of external parties. It allows businesses to validate the balances they hold or are owed and identify any discrepancies or errors that must be addressed. This process enhances the overall reliability and credibility of financial statements.

- Detecting Errors and Fraud: Account Confirmation plays a crucial role in detecting errors, omissions, or even fraudulent activities. Companies can identify discrepancies by comparing their records with those of external stakeholders, such as incorrect postings, unauthorized transactions, or missing balances. This helps in promptly investigating and rectifying any anomalies.

- Strengthening Auditing Procedures: Auditors heavily rely on balance confirmation as an essential tool during the auditing process. By obtaining confirmations from external parties, auditors gain independent verification of the balances, transactions, and obligations recorded in the financial statements. This enhances the accuracy and thoroughness of the audit, assuring stakeholders.

- Enhancing Transparency and Accountability: Account Confirmation promotes transparency and accountability in financial transactions. It demonstrates a company’s commitment to open communication and fosters stakeholder trust. By obtaining confirmations, businesses can demonstrate that their financial information is accurate and reliable, enhancing the confidence of investors, lenders, and other stakeholders.

- Resolving Discrepancies: Account Confirmation allows companies to address any discrepancies or disagreements with external parties promptly. If a stakeholder provides a different balance or raises a concern, it will enable both parties to investigate and resolve the issue on time. This helps maintain healthy business relationships and avoids potential disputes in the future.

- Compliance with Regulations and Standards: Many regulatory bodies and accounting standards require using balance confirmation as a standard practice. By adhering to these requirements, companies ensure compliance with legal and regulatory frameworks, thereby avoiding penalties and maintaining their reputation.

In this digitized age, automation for balance confirmation tasks is necessary. By leveraging automated systems, businesses can streamline their confirmation procedures, reduce manual efforts, enhance data security, and improve their financial operations’ efficiency and effectiveness.

Firmway offers a one-of-its-kind balance confirmation solution. It is a user-friendly tool that constantly monitors your customers and vendors, protecting you from unforeseen surprises. With its intuitive interface, the software significantly increases third-party response rates without manual intervention. Experience the ease and effectiveness of Firmway’s balance confirmation solution now!

How AI is Revolutionizing the Audit Industry :-

How AI is Revolutionizing the Audit Industry :-

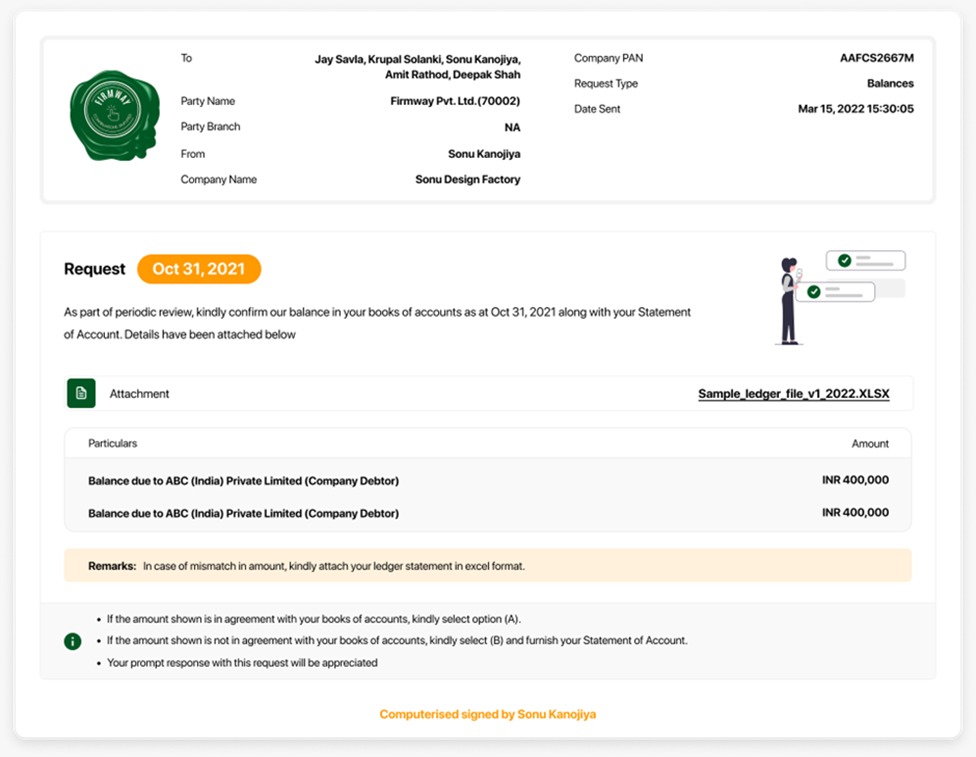

Illustrative Balance Confirmation Letter to be Sent to Debtors Negative Form

Illustrative Balance Confirmation Letter to be Sent to Debtors Negative Form

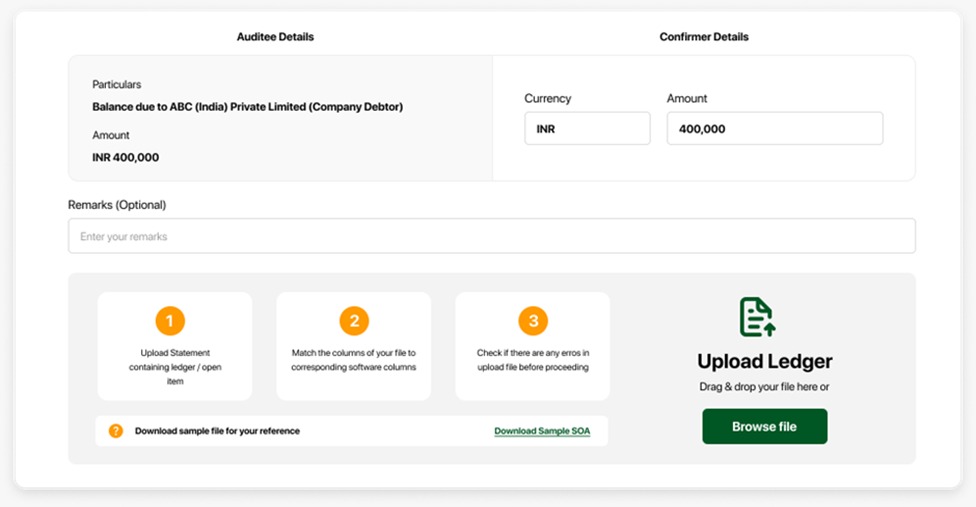

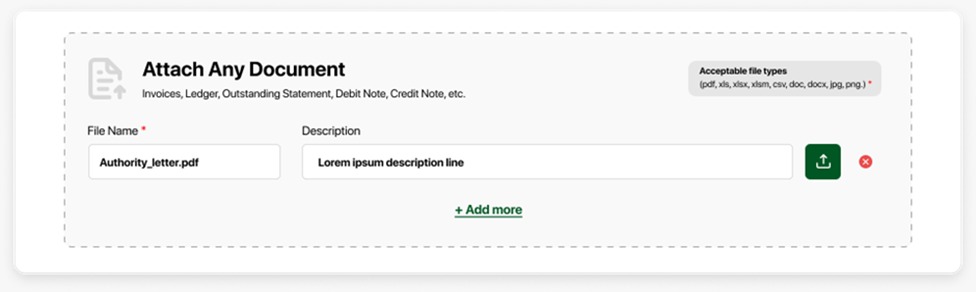

How do we do it?

How do we do it?

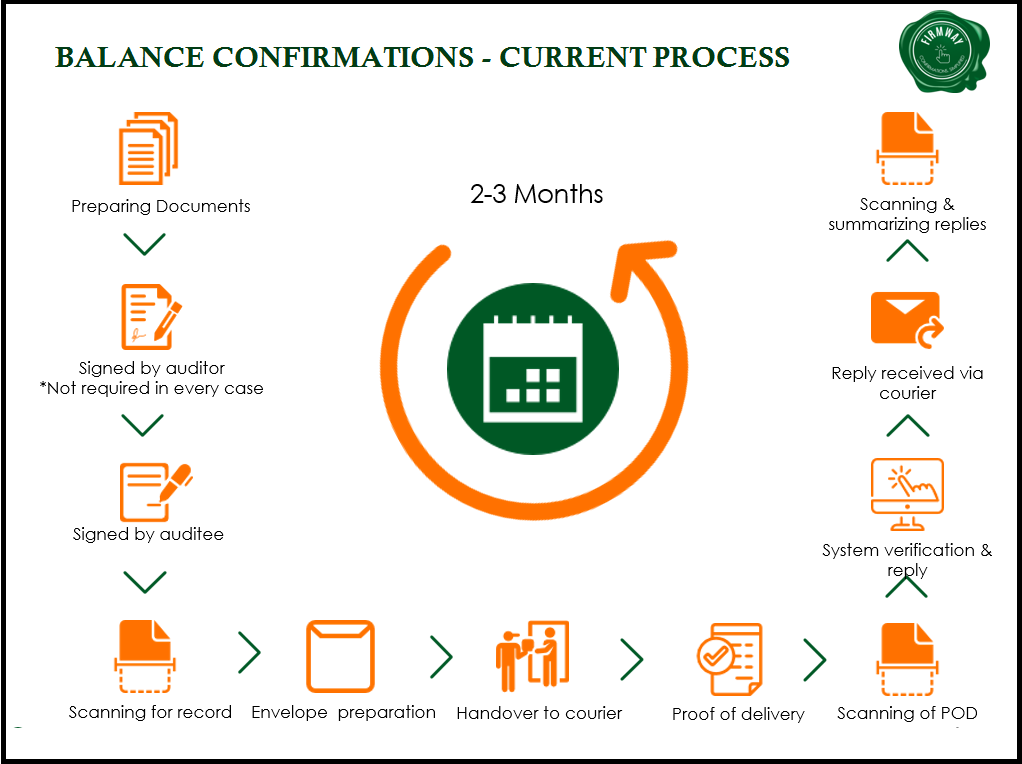

The Daunting Task of Manual Balance Confirmations

The Daunting Task of Manual Balance Confirmations